r3.0 Public Comment Letter to EFRAG (regarding ESRS): Sustainability Reporting requires integration of thresholds and allocations

From:

Bill Baue, Senior Director

Ralph Thurm, Managing Director

r3.0 (Redesign for Resilience & Regeneration)

Alexanderstrasse 7

10178 Berlin, Germany

To:

Ms Kerstin Lopatta

Acting Chair

Sustainability Reporting Board

European Financial Reporting Advisory Group (EFRAG)

35 Square de Meeûs

1000 Brussels

Belgium

8 August 2022

Dear EFRAG,

We respectfully submit this Public Comment Letter on the Exposure Drafts (EDs) of the European Sustainability Reporting Standards (ESRSs) to the European Financial Reporting Advisory Group (EFRAG) with an intention of strengthening the existing Drafts, which contain many strong elements, but also, importantly, contain a fatal flaw — namely, its inconsistent (and most often inexistent) integration of sustainability thresholds, and allocations of responsibility for respecting these sustainability thresholds (across ecological, social, and economic dimensions) at the organisational level (i.e., the level of the “undertaking,” to use EFRAG’s language). Ecological, social, and economic thresholds define sustainability, and allocations enable assessment of performance at the organisational level in terms of respecting these thresholds, which typically apply at higher scales (e.g., macro systemic levels).

In other words, sustainability reporting requires integration of thresholds and allocations.

Accordingly, the ESRSs will need to integrate thresholds and allocations comprehensively, if EFRAG wishes for the ESRSs to be authentic Sustainability Reporting Standards.

Background: The Birth of Sustainability Context (Thresholds and Allocations)

To better understand the necessity of the ESRSs integrating thresholds and allocations, it is useful for us to introduce ourselves. We are the Senior Director (Bill Baue) and Managing Director (Ralph Thurm) of r3.0,[1] which stands for Redesign for Resilience & Regeneration, a not-for-profit gGmbH registered in Berlin, which focuses on advocating for thresholds and allocations specifically, and more generally for the overarching framework of Context-Based Sustainability (CBS).[2]

CBS takes its name from the Sustainability Context Principle, introduced in 2002 in the second generation (G2) of the Global Reporting Initiative (GRI) Sustainability Reporting Guidelines. At that time, r3.0 Managing Director Ralph Thurm served as Chief Operating Officer of GRI, and led the Principles Development work stream for G2, and so held significant responsibility for the development of the Sustainability Context Principle.

The Sustainability Context Principle states that:

“…sustainability reporting draw significant meaning from the larger context of how performance at the organisational level affects economic, environmental, and social capital formation and depletion at a local, regional, or global level.

…simply reporting on the trend in individual performance (or the efficiency of the organisation) leaves open the question of an organisation’s contribution to the total amount of these different types of capital.

…placing performance information in the broader biophysical, social, and economic context lies at the heart of sustainability reporting.

…reporting organisations should consider their individual performance … in the context of the limits and demands placed on economic, environmental, or social resources at a macro-level.”[3] [Emphasis added]

Sustainability Context Group Seeks to Fill Sustainability Context Gap

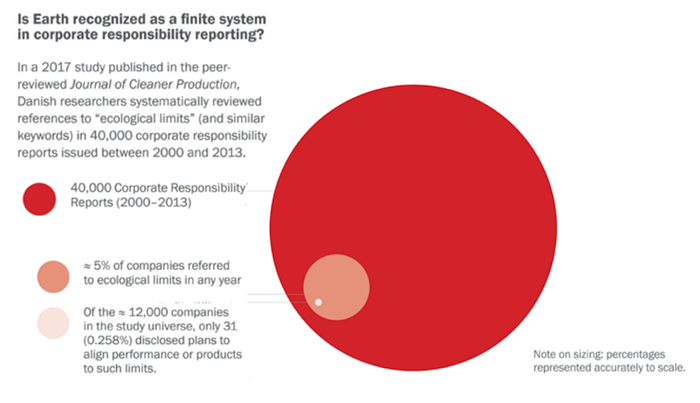

A decade later (in 2012), r3.0 Senior Director Bill Baue co-founded (with Mark McElroy, Founding Director of the Center for Sustainable Organizations) the Sustainability Context Group,[4] an informal network that advocated for more robust implementation of the Sustainability Context Principle. This move resulted from frustration over the lack of implementation of the Sustainability Context Principle, a dynamic that was later scientifically documented in a peer-reviewed study that found only 5% of sustainability reports issued between 2000 and 2013 mentioned ecological limits (i.e., thresholds), and a mere 0.258% actually implemented respect for ecological thresholds (i.e., in product design or corporate strategy).[5] See Figure 1.

To crystallize understanding of the necessity of integrating the Sustainability Context Principle in sustainability reporting, Baue interviewed GRI Co-Founder Allen White in 2013. He stated:

“Sustainability requires contextualization within thresholds. That’s what sustainability is all about.”[7] [Emphasis added]

White further expounded that

“an initiative that purports to be a sustainability initiative could not simply frame its work along the lines of, shall we say, incremental performance assessment. That is, companies that were improving each year in regard to water management, energy management, living wages and occupational health and safety should be recognized in the evolving … framework. But incrementalism alone, at the end of the day, [is] insufficient to be faithful to a sustainability reporting framework. [One] would have to take a further step and include [guidance] that would call for assessing — in addition to disclosures on backward-looking benchmarks, peer group comparisons, and improvements against a company’s own goals — performance against thresholds and limits.”[8] [Emphasis added]

White concluded:

“We don’t have decades to get serious about Context in light of the ecological and social perils that lie ahead. I think the time for procrastination has passed and the time for aggressive movement is upon us. The world is issuing a collective wake-up call on the issue of thresholds and limits. We’ve lost precious time dawdling in the last decade. We can’t afford another decade of the same.”[9] [Emphasis added]

Unfortunately, the sustainability reporting field ended up spending the last decade continuing to dawdle on Sustainability Context. The Sustainability Context Group submitted Public Comment Letters throughout the past decade encouraging standard-setters to integrate robust guidance on implementing Sustainability Context (i.e., thresholds & allocations), but these reasoned pleas fell on deaf ears.[10]

We are concerned that EFRAG and the ESRSs fall into this same dynamic of failing to sufficiently integrate Sustainability Context / thresholds & allocations.

Sustainable Finance Taxonomy Defines Thresholds on Political Expedience, not Biophysical Reality

We at r3.0 identified the emergence of this dynamic as early as 2019, in the development of the European Commission Sustainable Finance Taxonomy, as documented in our 2020 Sustainable Finance Blueprint:

“We like to first point out one quote from the June 2019 [EC Sustainable Finance Taxonomy] report that is a posterchild of the problem of sustainability context: the use of term threshold in a non-scientific way, something that corrupts the complete intention of the ‘Sustainable Finance’ idea:

‘To ensure the broadest usability of the Taxonomy possible, the TEG had to arbitrate between granularity and flexibility as well as between complexity and clarity. A very granular Taxonomy, which uses precise metrics and thresholds, is expected to provide clarity and to minimize the risk of greenwashing. Nevertheless, there is a risk that requirements that are too granular and stringent lower the willingness of stakeholders to take up the Taxonomy, due mainly to the costs to access the necessary data and adapting their internal processes. On the other hand, more flexibility in the definition of screening criteria may facilitate the use of the Taxonomy but increase significantly the risk of divergent interpretations and greenwashing. Another challenge regarding the definition of the screening criteria is setting the adequate level of thresholds. Setting too low or too high thresholds, which do not reflect best market practices, would undermine the Taxonomy’s ultimate goal of redirecting financial flows towards sustainable investments. Consequently, the selection of the Taxonomy’s thresholds has been carefully considered, based on existing standards and consultation processes with experts in the relevant sectors.’[11]

This explanation makes it clear that the EU Technical Expert Group is approaching thresholds not as biophysical realities that must be abided in order to achieve sustainability in the real world, but rather as political variables open to negotiation amongst those with diverse positions of power. Therefore, it’s vital to understand that the term “thresholds” used throughout the 400+ page document is not sustainability thresholds, but rather thresholds as defined to “reflect best market practices” with the “ultimate goal of redirecting financial flows towards sustainable investments.” Of course, this raises the question of just how those investments can possibly be ‘sustainable’ if the thresholds used to measure them are divorced from biophysical reality?”[12] [Emphasis added]

The fact that the EC Sustainable Finance Taxonomy compromised the integrity of its definition of thresholds sets a dangerous precedent in terms of other EC initiatives — such as the Corporate Sustainability Reporting Directive (CSRD), which the EFRAG ESRSs operationalize.

Biodiversity and Ecosystems ESRS Defines Thresholds and Allocations Properly

This brings us to the current Exposure Drafts of the ESRSs. We will start on a positive note — with the singular instance in which one of the ESRS documents — namely, E4 on Biodiversity and Ecosystems — integrates thresholds and allocations (i.e., integrates authentic Sustainability Context). Specifically, under Disclosure Requirement E4–3 — Measurable targets for biodiversity and ecosystems, E4 contains the following required disclosure [13]:

“how the targets respect and are in alignment with ecological thresholds (e.g. the biosphere integrity and land-system change planetary boundaries[xiii]) and allocate responsibility for respecting these thresholds to the organisational level.”[14] [Emphasis added]

This text demonstrates both a strong element of this particular Draft Standard (E4), and also a fatal flaw of all the other Draft Standards, as well as the overarching ESRS framework:

- The strength, clearly, is that this element explicitly integrates ecological sustainability thresholds, and furthermore calls for allocating “responsibility for respecting these thresholds to the organizational level,” thereby integrating Sustainability Context, a prerequisite for all sustainability reporting;

- The fatal flaw, however, is that this integration of thresholds and allocations (i.e., Sustainability Context) is applied only to this Standard (E4), as if sustainability thresholds (and allocations to respect these thresholds to the organizational level) apply only in the case of the sustainability of biodiversity and ecosystems — which is self-evidently not the case. Sustainability Context (i.e., thresholds and allocations) should apply across the entire CSRD initiative, in particular the overall ESRS framework, including all 11 Standards (5 Environmental Standards — E1-E5; 2 Governance Standards — G1-G2; and 4 Social Standards — S1-S4), as well as the 2 General Standards (ESRS 1 and ESRS 2), and of course the bookending Cover Letter and EU Final Agreement. Unfortunately, our in-depth analysis of these documents finds scant evidence of integration of thresholds and allocations (i.e., Sustainability Context).

To be clear, this particular strength of E4 has its limitations: the document does not actually provide guidance on how the undertaking would implement thresholds and allocations — a necessary element, if EFRAG and the EC wish for undertakings to comply with its Standards in ways that would deliver sustainability.

That said, we much prefer E4’s inclusion of thresholds & allocations (i.e., Sustainability Context) over all the other ESRSs’ limited or lack of inclusion of thresholds & allocations (i.e., Sustainability Context).

ESRS 1 Defines Thresholds and Allocations Divorced from Sustainability

The most egregious instances of this elision comes in ESRS 1 and ESRS 2, where the General Principles that cascade across all Standards are established, as are the overarching General, Strategy, Governance, and Materiality Requirements.[15] These two documents should establish a Context-based approach to Sustainability Reporting that references sustainability thresholds and allocations of responsibility for respecting these thresholds to the organizational level.

Confoundingly, ESRS 1 is silent on sustainability thresholds & allocations. Even more confounding is that ESRS 1mentions the term “threshold” twice, yet each time the term is used in ways that have absolutely nothing to do with sustainability thresholds.

Specifically, ESRS 1 mentions materiality thresholds in ways that lend themselves exceedingly well to explicit integration of sustainability thresholds, yet the Exposure Draft fails to make this vital and necessary connection. Here is the first use of the term:

“The implementation of materiality implies the use of thresholds and/or criteria.”[16] [Emphasis added]

Following this, ESRS 1 provides more in-depth information on Impact Materiality and Financial Materiality, yet in neither instance does the Draft Standard mention sustainability thresholds — despite the fact that sustainability thresholds should apply to both Impact Materiality and Financial Materiality,[17] and despite the fact that sustainability thresholds literally define sustainability reporting, as we established earlier in this Public Comment Letter by quoting GRI Co-Founder Allen White). ESRS 1 states:

“Impact materiality is a characteristic of a sustainability matter or information in relation to an undertaking. A sustainability matter is material from an impact perspective if it is connected to actual or potential significant impacts by the undertaking on people or the environment over the short-, medium- or long-term. This includes impacts directly caused or contributed to by the undertaking in its own operations, products or services and impacts which are otherwise directly linked to the undertaking’s upstream and downstream value chain, and not limited to contractual relationships.”[18]

Note that sustainability thresholds are nowhere to be found in this definition of Impact Materiality. Nor, as we see below, in the definition of Financial Materiality, according to ESRS 1:

“Financial materiality in the context of sustainability reporting is a characteristic of a sustainability matter or information in relation to the undertaking. For the purposes of preparing sustainability reporting, a sustainability matter is material from a financial perspective if it triggers or may trigger significant financial effects on undertakings, i.e., it generates or may generate significant risks or opportunities that influence or are likely to influence the future cash flows and therefore the enterprise value of the undertaking in the short-, medium- or long-term, but it is not captured or not yet fully captured by financial reporting at the reporting date.”[19]

Ironically, immediately after these definitions, ESRS 1 reiterates its call for applying explicit materiality thresholds (i.e., thresholds separating material from immaterial issues), but it neglects to calls for applying explicit sustainabilitythresholds (i.e., thresholds separating sustainability from unsustainability):

“The undertaking shall establish explicit thresholds and/or criteria to determine when a disclosure is complied with through a statement ‘not material for the undertaking’.”[20] [Emphasis added]

Similarly, ESRS 1 mentions “allocation of resources,” but this reference does not address the allocation of vital capital resources that undertakings impact, and that stakeholders (or rightsholders, as we prefer to call them, due to their inherent rights) also rely on for their wellbeing. ESRS1 states:

“When reporting on implementation the undertaking shall describe how it manages its material matters and their related impacts, risks, and opportunities. This covers information on policies and targets, actions and action plans, and resources allocation, whereby … allocation of resources refers to the decisions taken to support actions and action plans with identified financial, human or technological resources.”[21] [Emphasis added]

The fact that undertakings impact vital capital resources that others rely upon for their wellbeing creates duties and obligations for undertakings to manage their impacts on these vital capital resources sustainably — a fact that goes unnoticed by ESRS 1.

Neither does the ESRS 1 mention of allocations refer to the allocation of responsibility to respect sustainability thresholds (as E4 makes clear is a necessary element of assessing sustainability). No, the ESRS 1 mention of allocations refers exclusively to the “financial, human, or technological resources” the undertaking uses as it “manages its material matters and their related impacts, risks, and opportunities.”[22] So, allocation in ESRS 1 refers not to the allocation of vital capital resources from the Commons, nor to the allocation of responsibility for sustainably managing impacts on these Common capitals.

ESRS 2 Compounds the Misdefinition of Thresholds and Allocations

While one might expect ESRS 2 (which addresses materiality in a more granular fashion) to integrate sustainabilitythresholds and allocations, unfortunately, the confounding dynamic of eliding sustainability thresholds and allocations only compounds, as the text literally uses the appropriate linguistic formulation, but applies it to the wrong actions. Specifically, ESRS 2 states:

“A description of the undertaking-wide structure with regard to sustainability matters, including allocation of responsibilities and reporting lines, up to the administrative, management and supervisory bodies, including the role of: i. management level senior executives; and ii. other employees at the operational level.

When the undertaking has or will put in place initiatives to modify its strategy and business model(s), in order to reduce or eliminate the risk or to benefit from the opportunity and/or in order to prevent and mitigate negative material impacts and enhance positive material impacts (see ESRS 2 Disclosure Requirements SBM 3 and 4) the undertaking shall make explicit reference to the allocation of responsibilities and to the organisational structure put in place to address related impacts, risks and opportunities.”[23] [Emphasis added]

Neither of the authors of this Public Comment Letter (Baue and Thurm) have much hair left on their heads, but you can imagine us pulling out what little hair we have left upon reading these paragraphs. ESRS 2 utilizes the term “allocation of responsibilities” in relationship to “sustainability matters,” but this refers to the allocation of responsibilities within the undertaking for decision-making; it does not refer to the allocation of responsibilities “for respecting these [sustainability] thresholds to the organisational level” (to quote from the proper formulation in E4), as this latter allocation takes place amongst and between different undertakings (i.e., organisations), who each have impacts on shared vital capital resources in the Commons, and so must identify their fair share of responsibility for respecting these sustainability thresholds, commensurate with their proportionate impacts on these vital capital resources (that others rely on for their wellbeing).

Our hair-pulling frustration continued with ESRS 2’s mention of thresholds, which comes tantalizingly close to E4’s proper formulation (“respect and are in alignment with ecological [sustainability] thresholds” — and, we would add, social and economic sustainability thresholds), but confoundingly apply a different formulation. Specifically, ESRS 2 uses the term “threshold” to refer to “impact materiality,” which we already know (via the quotation from ESRS 1) does not make reference to sustainability thresholds (i.e., the demarcation line between sustainability and unsustainability in ecological, social, and economic systems.) ESRS 2 states:

“The undertaking shall give a justification and appropriate evidence that the undertaking is not involved with the negative impacts through its activities or business relationships; or that the relative severity and likelihood of these impacts do not meet a threshold of impact materiality.”[24] [Emphasis added]

What makes this repeated neglect of applying sustainability thresholds and allocations to the ESRS definition of materiality especially confounding is that guidance exists to do just this — from the United Nations, no less. In 2019, the United Nations Research Institute for Social Development (UNRISD) published a Working Paper entitled Making Materiality Determinations: A Context-Based Approach.[25] This paper calls for determining materiality with

“reference to thresholds in the carrying capacities of vital capitals, and organization-specific allocations of the responsibility to create, preserve and/or maintain them with stakeholder well-being in mind.”[26]

Double Materiality is Insufficient; Context-Based Materiality is Necessary

Along these lines, while we loudly applaud EFRAG and the ESRSs for embracing “double materiality,” calling for accountability for both outside-in impacts and risks (how the world impacts the undertaking — which the ESRSs call “financial materiality”) and also inside-out impacts and risks (how the undertaking impacts the world — which the ESRSs call “impact materiality”), clearly double materiality alone is insufficient, because it fails to take sustainability thresholds and allocations explicitly into account. Materiality that truly takes sustainability into account calls for a context-based approach, which integrates sustainability thresholds and allocations.

We therefore strongly recommend that the EFRAG take the logical next step of integrating sustainability thresholds and allocations in its approach to materiality,

To be clear, however, we do not limit our recommendation to materiality when it comes to integrating sustainability and allocations. We believe that sustainability thresholds and allocations need to be integrated comprehensively, from the core to the periphery of sustainability reporting standards.

Impact Management Platform Endorses Sustainability Threshold and Allocations

We are not alone in this belief. Indeed, the Impact Management Platform, the most significant consortium of sustainability reporting standards globally, likewise endorses comprehensive integration of thresholds and allocations in impact assessment and management. In November 2021, the Impact Management Platform (IMP) emerged as a reconfiguration of the Impact Management Project, which sunsetted at the end of its predetermined lifespan, and launched its inaugural Website — which included a landing page dedicated to Thresholds and Allocations.[27] Given the significance of this endorsement, it warrants quoting the IMP Thresholds and Allocations landing page:

“Thresholds

A sustainable future relies on ensuring that no one falls short on life’s essentials, and that collectively we do not overshoot our pressure on Earth’s life-supporting systems. Societal or ecological thresholds identified by science help establish the foundations and ceilings that earth and society should seek to operate within to prevent harm to people and the natural environment.

From a measurement perspective, this means that outcomes for people are sustainable if they are within the acceptable range determined by societal thresholds, and outcomes for the natural environment are sustainable if they are within the acceptable range determined by ecological thresholds…

Thresholds are critical contextual reference points for organisations assessing whether an outcome is sustainable or unsustainable. They are distinct from other types of targets that organisations might set themselves which are not explicitly linked to a scientific assessment of what constitutes a sustainable outcome.

Allocations

Whenever an organisation uses a shared resource or is part responsible for preserving or producing one, a further step is required to establish a fair allocation of the responsibilities involved. This becomes an organisation-specific threshold through a process called translation…

Allocation is the process of apportioning the responsibility to maintain thresholds in fair, just and proportionate ways that are specific to an organisation, making them practical for the organisation to apply when setting their own targets for measuring and managing sustainability performance.[28]” [Emphasis added]

United Nations Gives Imprimatur to Thresholds and Allocations

The Impact Management Platform is not the only significant multilateral organisation to give its imprimatur to thresholds and allocations. Since 2018, the United Nations Research Institute (UNRISD) has been developing a set of Sustainability Development Performance Indicators (SDPIs) covering economic, environmental, social, and institutional areas that integrate thresholds and allocations, as well as assessment of transformation.[29]

In 2019, UNRISD published a Working Paper that introduced a three-tiered typology of sustainable development performance indicators, predicated on the Sustainability Quotient (S = A / N) that defines Sustainability as Actual Impacts on the carrying capacities of vital capital resources in the numerator over Normative Impacts on the carrying capacities of vital capital resources in the denominator.

“Tier One: Incrementalist Numeration

Numeration indicators focus on actual impacts, which include absolute indicators as well as “intensity” indicators that describe performance relative to a nonnormative counterpart (such as unit of production), and are therefore incrementalist by definition.

Tier Two: Contextualized Denomination

Denomination indicators contextualize actual impacts against normative impacts. Also known as “Context-Based” indicators, denominator indicators take into account sustainability thresholds in ecological, social, and economic systems, as well as allocations of those thresholds to organizations and other sub-system entities such as sectors, portfolios, or bioregional habitats.

Tier Three: Activating Transformation

Transformation indicators add transcontextual elements of implementation practices and policies (as well as more ephemeral emergence) to normative indicators in order to instantiate sufficient change within complex adaptive systems.”[30]

In 2020, UNRISD pilot tested the indicator set at a couple dozen enterprises globally.[31] Organizations that participated in the pilot testing project included large multinationals such as Anglo American and Manulife, and smaller social & solidarity economy enterprises, such as two Mondragon cooperatives and Vancity, as well as key multilaterals and intermediaries such as the Impact Management Project, World Bank and World Benchmarking Alliance.

One pilot company (GLS Bank) started implementing the Indicators even before the end of the pilot testing, integrating them into its 2020 Integrated Sustainability Report.[32]

The Synthesis Report summarizing the results of the pilot testing project documented two key outcomes:

- First, the pilot testing companies were able to implement essentially all of the indicators, demonstrating the feasibility of thresholds-based sustainability measurement and reporting;

- Second, the pilot testing companies embraced a context-based approach to materiality.

This demonstrates that taking a thresholds-and-allocations approach to sustainability measurement, management, and reporting is both necessary and feasible.

Conclusion: EFRAG ESRSs Must Embrace Sustainability Threshold and Allocations

There are many other areas in the Exposure Drafts that we could spotlight where sustainability thresholds and allocations are necessary, but currently absent. Perhaps most glaringly, ESRS E1 on Climate Change makes reference to the well below 2°C / aim for 1.5°C threshold of the Paris Agreement, but E1 fails to call for allocating this threshold to the organisational level. This is particularly confounding, seeing as robust methods for doing so have existed since 2006, when Unilever subsidiary Ben & Jerry’s first aligned its greenhouse gas emissions with an Intergovernmental Panel on Climate Change (IPCC) climate scenario for decarbonization in respect of the carbon budget.[33] And the Science Based Targets initiative has since emerged as a de facto standard for allocating respect for the carbon budget to the organisational level via alignment with climate science scenarios and decarbonization pathways.

Similarly, ESRS E2 on Pollution mentions “respective specific loads” when it comes to pollution, but it does not call for setting sustainability thresholds for pollution loads, despite the existence of approaches (such as the Total Maximum Daily Load (TMDL) concept from the US Environmental Protection Agency (EPA). E2 mentions the term threshold once is a somewhat relevant way, but it fails to call for allocations.

ESRS E3 on Water and Marine Resources mentions “positive impacts,” suggesting the existence of a threshold dividing positive (sustainable) from negative (unsustainable) impacts, but it fails to explain how undertakings would identify and measure “positive impact” in ways that align with sustainability thresholds.

Finally, ESRS S1 on Undertakings’ Own Workforce mentions “fair remuneration” but fails to align this with the threshold of a living wage. S1 also mentions a gender pay gap, but no norm or threshold of an acceptable or sustainable gap (presumably this would be zero gap). And similarly, S1 mentions a compensation ratio, but fails to define a norm or threshold of a sustainable compensation ratio.

As should be clear by now, the ESRSs have a significant opportunity to mature into authentic sustainability reporting standards. Accordingly, we conclude by strongly encouraging EFRAG to adopt a sustainability thresholds-and-allocations approach to the European Sustainability Reporting Standards.

Sincerely,

Bill Baue Ralph Thurm

Senior Director, r3.0 Managing Director, r3.0

[1]See https://www.r3-0.org/

[2] Wikipedia. n.d. Context-Based Sustainability. https://en.wikipedia.org/wiki/Context-Based_Sustainability

[3] Global Reporting Initiative. 2002. Sustainability Reporting Guidelines. Version 2.0 (G2). https://www.r3-0.org/wp-content/uploads/2020/03/GRIguidelines.pdf

[4] Sustainability Context Group. n.d. r3.0. https://www.r3-0.org/scg/

The Sustainability Context Group submitted a number of Public Comment Letters urging standard setters to embrace more robust integration of Sustainability Context. r3.0 has since taken on management of the Sustainability Context Group.

[5] Anders Bjørn, Niki Bey, Susse Georg, Inge Røpke, and Michael Zwicky Hauschild. 2017. Is Earth recognized as a finite system in corporate responsibility reporting? Journal of Cleaner Production. Volume 163. Pages 106–117. October 2017. https://www.sciencedirect.com/science/article/pii/S0959652615019204

[6] Ibid. Graphic Source: Bill Baue. 2019. Compared to What? A Three-Tiered Typology of Sustainable Development Performance Indicators From Incremental to Contextual to Transformational. United Nations Research Institute for Social Development (UNRISD). Working Paper 2019–5. 7 October 2019. https://www.unrisd.org/en/library/publications/compared-to-what-a-three-tiered-typology-of-sustainable-development-performance-indicators-from-incr

[7] Bill Baue. 2013. #SustyGoals 2: A Dialogue with Allen White of GISR, the Godfather of Sustainability Context (Part 2). Sustainable Brands. 8 November 2013. https://sustainablebrands.com/read/new-metrics/sustygoals-2-a-dialogue-with-allen-white-of-gisr-the-godfather-of-sustainability-context-part-2

[8] Bill Baue. 2013. #SustyGoals 2: A Dialogue with Allen White of GISR, the Godfather of Sustainability Context (Part 1). Sustainable Brands. 7 November 2013. https://sustainablebrands.com/read/new-metrics/sustygoals-2-a-dialogue-with-allen-white-of-gisr-the-godfather-of-sustainability-context-part

[9] Ibid.

[10] See https://www.r3-0.org/scg/ for copies of these Public Comment Letters.

[11] EU Technical Expert Group on Sustainable Finance. 2019. Financing a Sustainable European Economy: Taxonomy Technical Report. European Commission. June 2019. https://ec.europa.eu/info/sites/default/files/business_economy_euro/banking_and_finance/documents/190618-sustainable-finance-teg-report-taxonomy_en.pdf

[12] Bill Baue & Ralph Thurm. 2020. Blueprint 6: Sustainable Finance — Systemic Transformation to a Regenerative & Distributive Economy. r3.0. 8 September 2020. https://www.r3-0.org/wp-content/uploads/2020/09/r3-0-Sustainable-Finance-Blueprint-Final.pdf

[13] Footnote from the original E4 text: “A description of the nine planetary boundaries can be found here: https://www.stockholmresilience.org/research/planetary-boundaries/the-nine-planetary-boundaries.html"

[14] Project Task Force (PTF) of the European Sustainability Reporting Standards. 2022. [Draft] ESRS E4 Biodiversity and ecosystems. European Financial Reporting Advisory Group. Exposure Draft. April 2022. https://www.efrag.org/Assets/Download?assetUrl=%2Fsites%2Fwebpublishing%2FSiteAssets%2FED_ESRS_E4.pdf

[15] Project Task Force of the European Sustainability Reporting Standards. 2022. [Draft] ESRS 1: General principles. European Financial Reporting Advisory Group. Exposure Draft. April 2022. https://www.efrag.org/Assets/Download?assetUrl=%2Fsites%2Fwebpublishing%2FSiteAssets%2FED_ESRS_1.pdf

[16] Ibid.

[17] “Sustainability performance is totally analogous to financial capital measurement — profitability is a threshold that measures sustainability…” states Cabot Creamery Cooperative Director of Sustainability Jed Davis in a report on the pilot testing of thresholds-based sustainability performance indicators issued recently by the United Nations Research Institute for Social Development (UNRISD), which are discussed in more depth later in this Public Comment Letter:

Bill Baue with Ralph Thurm. 2022. Thresholds of Transformation: UNRISD Sustainable Development Performance Indicators Pilot Testing — Synthesis Report. United Nations Research Institute for Social Development. 20 July 2022. https://www.unrisd.org/en/library/publications/thresholds-of-transformation-unrisd-sustainable-development-performance-indicators-pilot-testing-syn

[18] PTF. 2022. ESRS 1. Op Cit.

[19] Ibid.

[20] Ibid.

[21] Ibid.

[22] Ibid.

[23] Project Task Force of the European Sustainability Reporting Standards. 2022. [Draft] ESRS 2 General, strategy, governance and materiality assessment. European Financial Reporting Advisory Group. Exposure Draft. April 2022. https://www.efrag.org/Assets/Download?assetUrl=%2Fsites%2Fwebpublishing%2FSiteAssets%2FED_ESRS_2.pdf

[24] Ibid.

[25] Mark McElroy. 2019. Making Materiality Determinations: A Context-Based Approach. United Nations Research Institute for Social Development (UNRISD). Working Paper 2019–6. 6 December 2019. https://www.unrisd.org/en/library/publications/making-materiality-determinations-a-context-based-approach

[26] Ibid. The quoted material included the following footnote in the original: “For more on how the concept of the carrying capacities of vital applies to materiality and to the specification of context-based metrics, see https://www.greenbiz.com/blog/2013/06/18/carryingcapacities-capitals"

We would also refer readers to a subsequent, more in-depth reference: Mark McElroy. 2022. Thresholds, Allocations and the Carrying Capacities of Capitals: Core Principles in Sustainability and Integrated Accounting. Center for Sustainable Organizations. https://www.sustainableorganizations.org/Thresholds-Allocations-CarryingCapacities.pdf

[27] Bill Baue & Ralph Thurm. 2021. Reporting Standard-Setter Network Embraces Sustainability Thresholds & Allocations: Launch of Impact Management Platform Website Represents a Watershed Moment. r3.0. 17 November 2021. https://r3dot0.medium.com/reporting-standard-setter-network-embraces-sustainability-thresholds-allocations-41d711c7269f

[28] Impact Management Project. 2021. Thresholds and Allocations. https://impactmanagementplatform.org/thresholds-and-allocations/

[29] United Nations Research Institute for Social Development (UNRISD). 2018–2022. Sustainable Development Performance Indicators (SDPIs). https://www.unrisd.org/en/research/projects/sustainable-development-performance-indicators

[30] Bill Baue. 2019. Compared to What? A Three-Tiered Typology of Sustainable Development Performance Indicators From Incremental to Contextual to Transformational. United Nations Research Institute for Social Development (UNRISD). Working Paper 2019–5. 7 October 2019. https://www.unrisd.org/en/library/publications/compared-to-what-a-three-tiered-typology-of-sustainable-development-performance-indicators-from-incr

[31] Baue &Thurm. 2022. op cit.

[32] GLS Bank. 2021. Integrated Sustainability Report 2020. https://nachhaltigkeitsbericht.gls-bank.de/files/About-GLS-Sustainability-Report-2020_English.pdf

[33] Ben & Jerry’s. 2006. 2006 Social & Environmental Assessment Report. Global Warming Social Footprint. https://www.benjerry.com/about-us/sear-reports/2006-sear-report#globwarmsocfootprint