By Bill Baue

Part 10 of a series on the r3.0 White Paper, From Monocapitalism to Multicapitalism — 21st Century System Value Creation.

Ultimately, value is to be interpreted by reference to thresholds and parameters established through stakeholder engagement and evidence about the carrying capacity and limits of resources on which stakeholders and companies rely for wellbeing and profit…

EY / IIRC, 2013[1]

A business model designed to maximize financial capital will not necessarily create the greatest value. From a value perspective, if a business model transforms capitals with a greater value (work capacity) than money into money, the transformation is inefficient. The result is more money but less value. In practical terms, this means the business model is producing less capacity to do work in the future. This paradox is at the root of neoclassical economics. Rather that capitalize resources it leads to an overall decapitalisation. More money but less capacity to bring about positive change. A paradox that eventually leads to a value crisis.

Peter Tunjic, 2018[2]

The intersection between impact measurement / management and value creation is like a busy crossroads that’s continually under construction, with the solution of an efficient and effective intersection seeming ever elusive. To shift metaphors, the attention seems focused on seeing the trees more clearly, and losing perspective on the forest as a whole.

The IIRC spearheaded recent efforts helping to provide greater clarity. In its 2013 International <IR> Framework, IIRC introduced a graphic endearingly called the “Octopus” (though in reality the “creature” has not eight but twelves tentacles!) that maps how business models transform the multiple capitals from inputs to outputs that produce outcomes, resulting in value creation (and diminution) over time.[3] (see Figure 12) This flowchart (similar to Sankey diagrams of material flows[4]) helped visually crystallize the role of the multiple capitals and organizational business models in the value creation process.

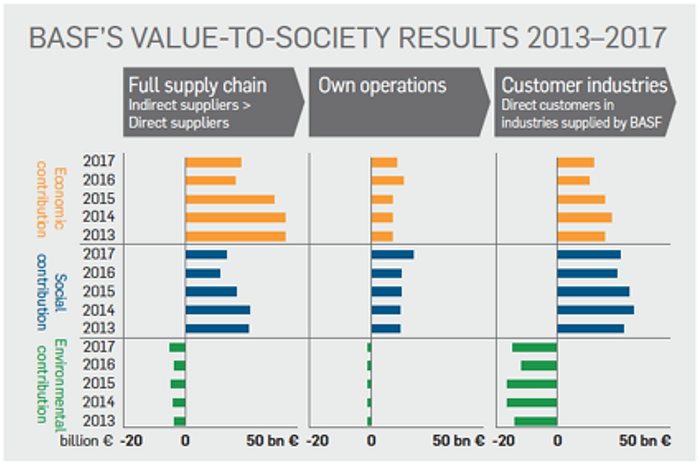

Subsequent work has extended this flowchart in useful ways. Work by the German chemical company BASF expanded from “outcomes” to “impacts,” a step that essentially introduces the question of attribution: “how much of the outcome would not have happened otherwise” (i.e. without the contribution of the organization in question). BASF also introduced a next step of “Value-to-Society” — in other words, what are the costs and benefits of these impacts to society at-large?[6] (See Figure 13)

This approach has gained significant traction in the field. The Impact Valuation Roundtable (BASF plus a dozen other big companies, collaborating under the umbrella of the World Business Council for Sustainable Development) embraced the BASF Value-to-Society approach. (See Figure 14) The naming of the roundtable spotlights the fact that the approach applies a “valuation” approach, employing monetization to express the impacts in terms that are both “fungible” and readily understood by market actors.

How does one place a valuation on impacts? For its part, BASF measures all its impacts (positive and negative), and puts a price on them (i.e. “monetizes” or “valuates” them) in order to be able to compare them in common terms.[9]

Note that all of BASF’s social and economic impacts are positive, whereas all its environmental impacts are negative. The Value-to-Society approach then “nets out” the impacts, enabling the company to claim that the positive social and economic impacts can offset (or “off-net”) negative ecological impacts.

In technical terms, BASF’s Value-to-Society methodology applies a “weak sustainability” approach that allows off-setting impacts on capitals (for example, degenerating natural capital to generate manufactured and social capital), instead of a “strong sustainability” approach that holds incommensurability and hence non-substitutability between capitals (natural capital cannot be “replaced” by social capital), and so precludes such capital offsetting.[12]

Despite this fundamental flaw, the Impact Valuation approach was sufficiently successful to enable its primary architect, Christian Heller of BASF, to spin it off into an independent initiative called the Value Balancing Alliance, which “aims to create a standardized model for measuring and disclosing the environmental, human, social and financial value companies provide to society.”[13] Heller explained the overall value of this kind of approach thus:

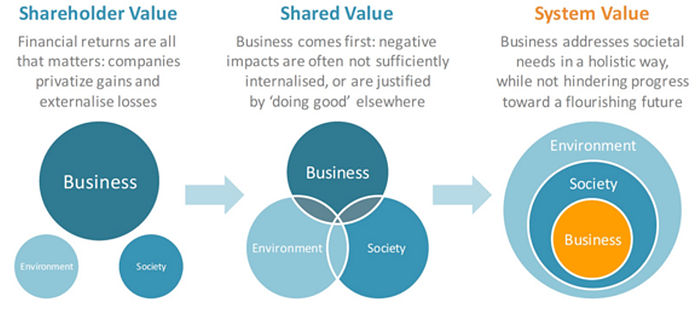

Moving from the traditional shareholder value concept to a “system value” approach, we truly value the impacts and interdependencies of society and business in a comprehensive system. This system serves as our foundation for shaping the future.[14]

This use of the term “system value” differs significantly from its origins. The concept was coined by Future-Fit Foundation Co-Founder and CEO Geoff Kendall, defining it broadly on the continuum from Shareholder Value (which prioritizes financial returns to shareholders) through Shared Value (which prioritizes financial gain that promotes social good, without accounting for social harm) to Systems Value (which views value holistically, aligning business value with social and ecological value).[15]

The Future-Fit Foundation promulgates the Future Fit Business Benchmark, a framework that calls for companies to reach “a set of environmental and social thresholds that constitute the extra-financial break-even point for value creation, across the Triple Bottom Line.” As suggested in the graphic, this falls within a “Requirement for Society” that constitutes “System Conditions defining the thresholds within which society must operate to protect the possibility of a flourishing future.”[16]

In other words, creating System Value requires operating (at the micro / company level and the macro / systems levels) within ecological, social, and economic thresholds. System Value is therefore explicitly distinct from Impact Valuation, which operates without any reference to ecological, social, and economic thresholds.

In the real world, human benefit does not erase adverse environmental impact; quite the opposite: human thriving often comes at the cost of the environment, so true thriving must be redefined to align with vibrant environmental viability. Viewed through this lens, unabated environmental erosion (as is evidenced by the five-year results from BASF) eats away the future foundation that social benefit is built upon, undermining the system.

Creating System Value thus requires that systems thrive in healthy cycles of resource regeneration. Well-functioning systems create value from sufficiently abundant capital stocks to generate ongoing resource flows. So, System Value creation requires cycling resources within their carrying capacities.

The shortcomings of Impact Valuation (and similar doctrines and regimes) are two-fold, when it comes to bona fide value creation (i.e. taking a systemic perspective):

1. They do not attend to normative thresholds of the carrying capacities of capitals; and

2. Their application of monetization, intended to create comparability, actually distorts accurate perception of the non-fungibility of the capitals. Or, perhaps more accurately, that the transmission of value between and amongst the multiple capitals is not as simplistic as monetization captures.

Peter Tunjic, an Australian corporate lawyer who applies thermodynamic principles to corporate flows of energy and value, has formulated a theory of “capital dynamics,” which he defines as

the study of energy in its social form — value. The field examines the relationship between value, work, the forms of capital in which value accumulates, the entropic and other qualities of each form of capital and the conversion of value between different forms.[17]

Mr. Tunjic holds that “value is stored in capital … [it] is the energetic potential of a capital to do … the work of change.” He continues:

Value is created when one form of capital is transformed into another with greater potential value. This is called “capitalization.” Put simply, the output capital could do more work than the input capital (after the costs of transformation).[18]

A business model designed to maximize financial capital will not necessarily create the greatest value. From a value perspective, if a business models transforms capitals with a greater value (work capacity) than money into money, the transformation is inefficient. The result is more money but less value. In practical terms, this means the business model is producing less capacity to do work in the future.[19]

This false assumption — that transformation of non-financial capitals into financial capital represents a net-sum creation of value — represents an Achilles Heel of Monocapitalism. Mr. Tunjic continues:

This paradox is at the root of neoclassical economics. Rather than capitalize resources, it leads to an overall decapitalisation. More money but less capacity to bring about positive change. A paradox that eventually leads to a value crisis.[20]

If “capitalization” exists, so too must “decapitalization,” Mr. Tunjic reasons, as he explains in more depth thus:

Decapitalisation results from an inefficient conversions of capitals that decreases net value calculated across all capitals. A theory of capitalism based on neo-classical economic assumptions is a recipe for the growth of financial capital and the decline of other capitals [because] … there is less value available to do the work of positive change. Capitalism cannot defy the second law of thermodynamics…

For if the other … capitals invested for [financial] profit hold greater value than the resulting financial capital, there is no capitalisation or increase in value. The net effect is logically a reduction in total value or “decapitalisation”. Decapitalist efficiency turns out to be a highly inefficient way to allocate the worlds limited resources. Exchanging the worth-more for the worth-less is fool’s alchemy.[21]

Mr. Tunjic’s notions support the idea of System Value Creation in transcapital terms, in the sense of optimizing the overall capital stocks and flows — instead of creating illusory value through overall capital stock and flow depletion for the sake of propping up growth of a singular (financial) capital. This “capital dynamics” approach complements a thresholds-and-allocations-based carrying capacities of the capitals approach to System Value Creation.

One of the stronger definitions of System Value Creation doesn’t even mention systems! In the build-up to its 2013 <IR> Framework, IIRC enlisted partners to produce a set of background papers through a multistakeholder engagement process. EY pulled together a Background Paper on Value Creation that ended with the following final paragraph (the famous “Paragraph 58,” as it’s known in the Multicapitalism community):

Ultimately, value is to be interpreted by reference to thresholds and parameters established through stakeholder engagement and evidence about the carrying capacity and limits of resources on which stakeholders and companies rely for wellbeing and profit… Interconnections between corporate activity, society and the environment and the purpose of the corporation should therefore be understood in terms of what the corporation, society and the environment can tolerate and still survive — that will be the main determinant of value. The challenges will be to reach agreement at corporate, national and international levels on what those thresholds and limits are, how the resources within those limits should be allocated, and what action is needed to keep activity within those limits so that value can continue to be created over time.[22] [emphasis added]

This systemic interpretation of value creation was potentially too far ahead of its time in 2013, as the <IR> Frameworkintegrated the multiple capitals without grounding in thresholds, allocations, carrying capacities, resource limits, and well-being (as articulated in this paragraph).[23] Indeed, as comprehensive as this paragraph is on elements of Multicapitalism, it actually doesn’t make reference to the capitals. Multicapitalism thus builds on the strong foundation of Paragraph 58, and extends it further.

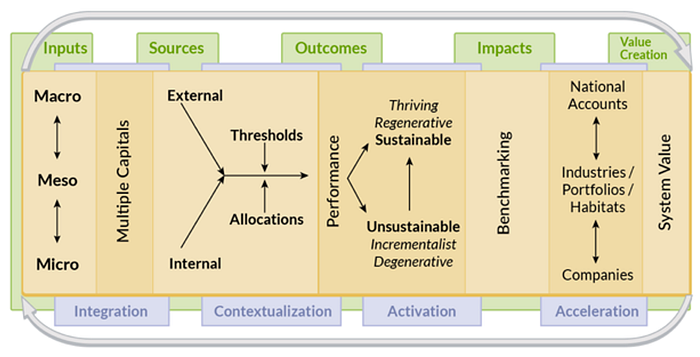

r3.0 produced a visual representation of System Value Creation in its Transformation Journey Blueprint, specifically addressing the question of data flows in a Multicapitalist application. Labeled the Integral Data Flowchart, it integrates information across the multiple capitals, from both internal and external sources (at the micro, meso, and macro levels) that assesses performance within sustainability thresholds and allocations in order to create System Value.

[1] EY, Value Creation Background Paper, International Integrated Reporting Council, July 2013. https://integratedreporting.org/wp-content/uploads/2013/08/Background-Paper-Value-Creation.pdf

[2] Peter Tunjic, “Capital & Capitalisation,” OnDirectorship, 24 August 2018. http://ondirectorship.com/ondirectorship/6g3hjaczsstaj96egyb6sr6rxzy8cs

[3] IIRC, op cit.

[4] “Sankey diagram,” Wikipedia. https://en.wikipedia.org/wiki/Sankey_diagram; via Peter Tunjic, “Towards a New Science of the Corporation,” OnDirectorship, 3 October 2019. http://ondirectorship.com/ondirectorship/2019-2-2da7a

[5] Ibid.

[6] BASF, We Create Value, undated. https://www.basf.com/global/en/who-we-are/sustainability/we-drive-sustainable-solutions/quantifying-sustainability/we-create-value.html

[7] Ibid.

[8] Impact Valuation Roundtable, Operationalizing Impact Valuation: Experiences and Recommendations by Participants of the Impact Valuation Roundtable, White Paper, March 2017. http://docs.wbcsd.org/2017/04/IVR_Impact%20Valuation_White_Paper.pdf Note that this graphic essentially “cuts-and-pastes” the BASF Value-to-Society approach.

[9] Christian Heller (BASF), “Value To Society — A Balanced Approach To Measuring Business Impact,” Global Goals Yearbook 2019, UN Global Compact, 2019. https://www.basf.com/global/documents/en/sustainability/management-goals-and-dialog/networks/global-compact/Global%20Goals%20Yearbook_2019_BASF_2019-08-05.pdf

[10] Ibid.

[11] Ibid.

[12] Jérôme Pelenc, Jérôme Ballet & Tom Dedeurwaerdere, Weak Sustainability versus Strong Sustainability, Brief for United Nations Global Sustainable Development Report, 2015. https://sustainabledevelopment.un.org/content/documents/6569122-Pelenc-Weak%20Sustainability%20versus%20Strong%20Sustainability.pdf

[13] “About Us,” Value Balancing Alliance. https://www.value-balancing.com/about-us/

[14] Heller 2019, op cit.

[15] Future Fit Business Benchmark, Creating System Value, Concept Note, April 2017. https://futurefitbusiness.org/wp-content/uploads/2017/04/Future-Fit-Business-Benchmark-Creating-System-Value-Concept-Note-V1.pdf; Stephanie Bertels contributed to the development of the concept of System Value in conversations with Geoff Kendall dating back to this same time period, and integrated the concept into subsequent work with the Embedding Project. Stephanie Bertels & Rylan Dobson, Embedded Strategies for the Sustainability Transition: Setting Priorities and Goals Aligned with Systems Resilience, The Embedding Project, April 2020. https://embeddingproject.org/pub/resources/EP-Embedded-Strategies-for-the-Sustainability-Transition.pdf

[16] Future Fit Business Benchmark, Methodology Guidance, Release 2.1.4. August 2019. https://futurefitbusiness.org/wp-content/uploads/2019/08/FFBB-Methodology-Guide-R2.1.4.pdf

[17] Peter Tunjic, “Towards a New Science of the Corporation,” OnDirectorship, 3 October 2019. http://ondirectorship.com/ondirectorship/2019-2-2da7a. Thanks to r3.0 Advocation Partner Henk Hadders for pointing us to the work of Mr. Tunjic.

[18] Peter Tunjic, “Social Purpose without Social Responsibility : Rethinking the Corporation,” OnDirectorship, 10 February 2018. http://ondirectorship.com/ondirectorship/2018-2

[19] Peter Tunjic, 24 August 2018 , op cit.

[20] Ibid.

[21] Tunjic, 10 February 2018, op cit.

[22] EY, op cit.

[23] For example, the International <IR> Framework mentions “allocations” extensively in relation to resources (a term closely related to capitals), but not in relation to thresholds, which is the vital question. And well-being in mentioned in relation to social capital, but not as an overarching “ultimate ends.”

[24] Bill Baue, Data Blueprint — Data integration, contextualization & activation for multicapital accounting, r3.0, 2017.https://www.r3-0.org/wp-content/uploads/2019/07/R3-BP3.pdf

Here’s the link to Part 9: