What Are Thresholds & Allocations, and Why Are They Necessary for Sustainable System Value Creation?

By Bill Baue and Ralph Thurm

This is part 8 of the Reporting 3.0 series that highlights the ‘burning questions’ of Boards and Sustainability Professionals why we need Reporting 3.0 and what it aims to deliver with its Blueprints on Reporting, Accounting, Data and Integral Business Model Design.

What’s the issue?

Thresholds and allocations are easiest to understand by thinking of doughnuts and pies. Seriously.

Oxford Economist Kate Raworth popularized the idea of environmental and social thresholds by envisioning a doughnut: its outer edge represents “ecological ceilings” (i.e. Planetary Boundaries), or “do-not-exceed” limits of resource use beyond which natural systems start to collapse; its inner edge represents “social foundations,” below which societal systems start to founder[i].

And a “slice of the pie” is the best way to envision allocations, or a proportionate share (slice) of the full stock of a resource (pie). Think of water in a watershed, which needs to account for natural processes (e.g. evaporation; plant, animal & human consumption, etc…) before being divvied up between commercial / industrial users.

But now that you know what thresholds & allocations are, so what? How do they help us better understand how best to use our shared resources in ways that ensure their ongoing availability?

The idea of thresholds & allocations isn’t new. In fact, the concepts grew out of the notion of “capitals” as stocks of resources that generate productive flows, which are vital to support well-being (see below for a visual overview of the history of novel contributions to this thinking).

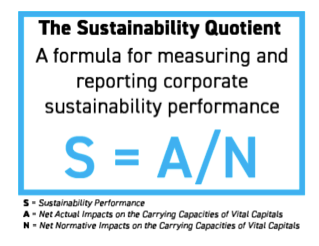

The key to achieving sustainability is to respect the carrying capacities of the capitals, as Reporting 3.0 Advocation Partner Mark McElroy established in his 2008 Doctoral Dissertation (applying the carrying capacities concept from the field of ecology). And McElroy also proposed a Sustainability Quotient for expressing thresholds, whereby sustainability (S) equals actual impacts (A) over normative impacts (N) — think carbon footprint over carbon budget.

And Reporting 3.0 notes that most practice in the so-called sustainability space (think CSR, ESG, etc…) amounts to numerator-only work, focused on incremental improvement that falls short of sustainability thresholds. As Reporting 3.0 Steering Board Member Brendan LeBlanc of EY notes, “the only thing more dangerous than no progress is the illusion of progress.” We at Reporting 3.0 also like to point out that thresholds and allocations are always being employed (resources always have upper or lower limits of viability, and use of a shared resource alwaysrequires parsing it out); the main question is how consciously resources are used and shared.

The key “marriage” of thresholds & allocations started with the Global Reporting Initiative (GRI) Sustainability Reporting Guidelines in its second generation (G2) released in 2002, which introduced the Sustainability Context Principle that tied micro-level organizational impacts on the multiple capitals to macro-level economic, social, and ecological systems viability. Ideally, this would have inspired companies to make this vital micro/macro link in their management, performance, and reporting in order to operationalize sustainability.

Unfortunately, a 2017 study of 40,000 sustainability reports issued since then found that only 5% make any mention of ecological limits, and only 31 of 9,000 reporting companies (0.3%) integrate such limits into their strategy and product development. Reporting 3.0 calls this the Sustainability Context Gap.

What can you do about it?

In its 2015 Raising the Bar report, UNEP succinctly summarizes what companies can do:

All companies should apply a context-based approach to sustainability reporting, allocating their fair share impacts on common capital resources within the thresholds of their carrying capacities.

A number of initiatives have spawned in the past decade to help operationalize thresholds and allocations:

- Employ Context-Based Metrics, such as Science Based Targets for greenhouse gas emissions reductions and Context-Based Water Stewardship Targets;

- Implement the UN Guiding Principles on Business & Human Rights;

- Utilize the Vital Capital Index in agriculture and assess synergies between sustainability impacts;

- Consult the Embedding Project’s Road to Context for guidance;

- Set “break even” and “positive pursuit” goals using the Future Fit Business Benchmark;

- Apply systems-level considerations and measure influence in investment decisions, as advocated by The Investment Integration Project;

- Conduct scenario analysis (with guidance at the TCFD Knowledge Hub) and produce transition plans to <2°C business models (as advocated by Preventable Surprises);

- Use the MultiCapital Scorecard.

In additions to these actions, Reporting 3.0 provides a comprehensive approach to applying thresholds & allocations through a number of fit-to-purpose tools:

- Mapping: The Reporting 3.0 Strategy Continuum (covered in Part 5 of this series) enables plotting of practices, impacts, business models, etc. on the spectrum from incremental improvement through sustainability (defined by thresholds and allocations) to regeneration and thriving;

- Implementation: The Reporting 3.0 Integral Materiality Process (covered in Part 6 of this series) applies thresholds and allocations in its context-based approach to materiality;

- Governance: The UNEP Raising the Bar report also recommends: Multilateral organizations should collaborate to create a global governance body of scientists, governments, businesses, NGOs and other stakeholders to provide guidance on methodologies for determining ecological (and social) thresholds, as well as guidance on approaches to allocations, all of which are broadly applicable to the business level.

Reporting 3.0 is enacting this recommendation by establishing the Global Thresholds & Allocations Council (GTAC) with a 3-prong mission:

- Identify thresholds & norms for sustaining the carrying capacities of systems-level capital resources in the commons that are vital to stakeholder wellbeing, based on a comprehensive review of research in physical and social sciences and practice in the field.

- Design and validate allocation methodologies that apportion fair share responsibility for jointly preserving and enriching capital resources vital to stakeholder wellbeing.

- Disseminate consensus-based thresholds/norms/allocations with “off-the-shelf” ease-of-use in mind to facilitate global mainstreaming of such practices.

What will you have achieved afterwards?

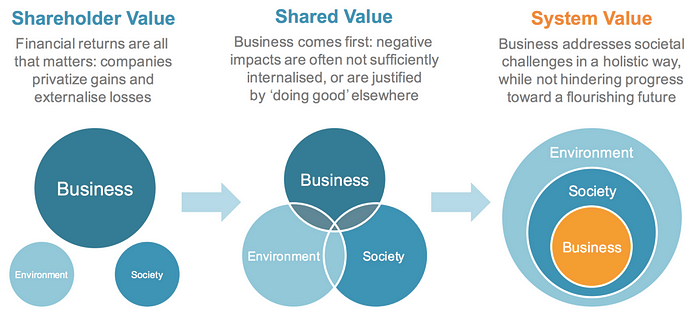

Application of thresholds and allocations is a necessary precondition for achieving truly sustainable organizations (at the micro level), industry sectors, investment portfolios and bioregional habitats (at the meso level), and economic, societal, and ecological systems (at the macro level). Indeed, thresholds & allocations approaches enable fulfillment of the transition from shareholder value creation to shared value creation (which aligns financial and social value creation while overlooking value destruction) to system value creation– which harmonizes financial value creation with the enhancement of social and ecological systems in which the economy operates.

What question will we discuss next time?

How Can New Lenses of Risk Help Ignite Breakthrough Transformations?

[i]The idea of outer and inner limits was first proposed by Barbara Ward in the Cocoyoc Declarationat a 1974 joint UNEP / UNCTAD Symposium.

Please add your feedback, the authors Ralph Thurm and Bill Baue of Reporting 3.0 will look at all responses. Don’t forget to ‘wave’ if the above resonated with you ;-).

[Context of this series: The sum of these articles form the basis of an Implementation Guide that summarizes the total value of Reporting 3.0 in implementing a future-ready sustainability strategy and disclosure approach, in line with the idea of a Green, Inclusive and Open Economy. By posting these articles here Reporting 3.0 seeks feedback in the writing process of the final document, to be released as Blueprint 5 at the 5th International Reporting 3.0 Conference in Amsterdam, The Netherlands, on June 12/13, hosted by KPMG, see www.2018.reporting.org]