Competition or Collaboration? The Ergodic Investor & Entrepreneur

By Bill Baue

Is it more advantageous to selfishly compete or altruistically collaborate?

This age-old question underpins some of the fiercest debates in science, and spills into other realms, including ethics, of course, but also, perhaps less intuitively (but arguably more importantly), business and investment. This latter intersection will be the eventual focus on this book review of Graham Boyd and Jack Reardon’s The Ergodic Investor & Entrepreneur, after some creative detours en route. Graham will be speaking on it in the Common Good Governance Session at the 2023 International r3.0 Conference.

Living under the pervasive cultural influence of Richard Dawkins’ brilliant (but flawed) 1976 bestseller The Selfish Gene, you can be forgiven for mistakenly assuming the answer is exclusively selfish competition. The popularity of the book is only partly attributable to its brilliance, and primarily attributable to its channeling the prevailing zeitgeist of its day, with Dawkins’ brand of evolutionary theory converging with neoliberal-capitalism-on-steroids to mutually reinforce hyper-individualization that rejected an instrumental role for collectivism and beneficence.

The only evolutionarily relevant role of altruism is to spread the gene, a theory known as kin selection, which vehemently rejected the notion of group selection (or more precisely, the more robust variant of multilevel selection, named for the notion that natural selection can occur at multiple levels, beyond the genetic or kin level). This kin selection line of thinking was so pervasive that biologist Bernd Heinrich didn’t know what to think when he observed a large group of ravens sharing a food bonanza (a moose carcass) in backwoods Maine in 1984. After many years of painstaking scientific observation, beautifully documented in his 1989 book Ravens in Winter, Heinrich came to the unavoidable conclusion that ravens engage in altruistic behavior in ways that defy explanation by selfish gene and kin selection theories.

Heinrich ends the book on this jovial note:

“…sometimes when I am fanciful and envision ravens studying humans, I can’t help but wonder what they would make of some of our customs, and how they might arrive at scientific conclusions about them.”

As it turns out, in the intervening years since this publication, multilevel selection has effectively displaced the supremacy of selfish gene and kin selection theories, demonstrating that (as David Sloan Wilson and E. O. Wilson conclude their definitive paper on the topic):

“Selfishness beats altruism within groups. Altruistic groups beat selfish groups. Everything else is commentary.”

This quick review of the recent development in evolutionary theory sets the necessary foundations for understanding ergodicity as it applies to business and investment. In their new book The Ergodic Investor & Entrepreneur, Graham Boyd and Jack Reardon early on define ergodic strategies succinctly in an un-technical way, focusing first on its practical implications:

“It gives us a way of collaborating for our own benefit with groups we currently see as competitors.”

More on this momentarily, but let’s briefly consider the more technical definition of ergodicity itself.

“In any process with randomness, there are two ways of figuring out what to expect in the limit where all the randomness cancels itself out. Either you let time go to infinity in one system, or you average over infinitely many systems at a fixed time. If these two ways give the same answer the system is ergodic. But often the path matters, and the two answers are different. Then the system is non-ergodic.”

Translating this from mathematical mumbo jumbo, Boyd explained to me that classical economics essentially established itself on the basis of idealized, linearized, independent events (ergodic) leading to outcomes when actually, in the real world, history matters, and context matters. In other words, the real world is non-ergodic so the same events lead to different outcomes.

Boyd and Reardon craftily deploy a set of charts to clearly demonstrate how business models built on classical economic assumptions may actually be predestined to fail, even if the business plan looks good, precisely because of this gap between an idealized, linearized (ergodic) assumption, and our history-dependent, context-dependent non-ergodic reality.

After you wrap your head around this analysis, the next obvious question is: ok, so what’s your secret sauce for avoiding this real-world outcome?

In a nutshell, Boyd and Reardon advocate for bridging the gap between ergodic ideals and non-ergodic reality with strategies borrowed from Elinor Ostrom’s 1990 masterpiece Governing the Commons (which set the foundation for her 2009 Nobel Prize in Economics): treating both risk and opportunity as common pool resources.

In other words, an ergodic strategy calls for integrating collaboration into the landscape of competition, a proposition that is heretical to traditional capitalist thinking, but gains currency when considering the empirical evidence of multilevel selection.

Boyd and Reardon put it like this:

“While everything in this book is pure maths, and this pure maths makes clear that resource pooling is a winning strategy, it can only work if the different parties are disincentivized from eating each other, taking the money and running, or some other action that shuts down the pooling.”

This involves applying both competition and collaboration!

“The sweet spot for actual individual companies is somewhere in the middle: an adaptive blend of collaboration and competition.”

They get a bit more nuanced than this:

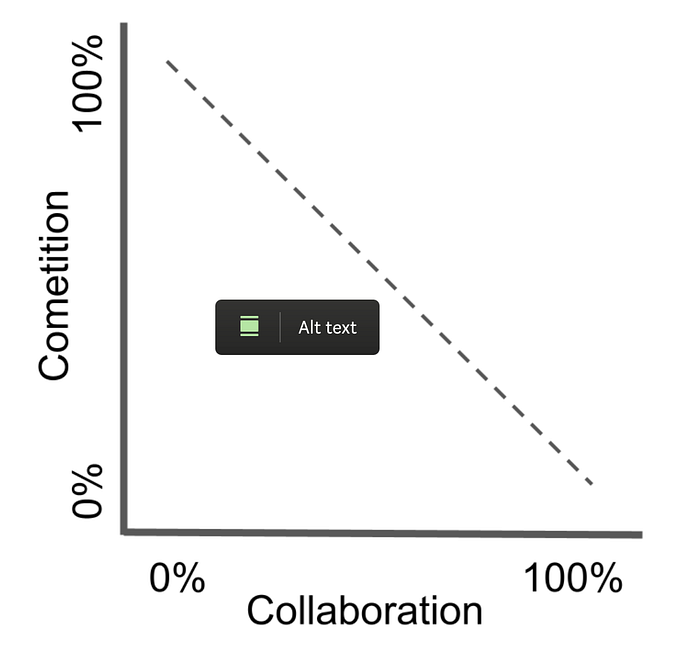

“Avoid thinking of your sweet spot as lying somewhere on the compromise straight line in any of the dimensions or variables relevant to your businesses. Rather, you have the entire area spanned to operate in, for example the two dimensions of competition and collaboration shown in Figure 6.1.”

“Executing a strategy that is at the sweet spot in the entire space (for example, one that has 80% collaboration and 80% competition) is where you have a competitive edge over others. The sweet spot typically lies outside the compromise line where competition plus collaboration must add up to 100%.

I find a delicious irony in this: ergodic strategies that out compete because they out collaborate!”

One instantiation of this approach is to apply both pooled losses (think of it as a kind of insurance) and pooled profits (think of it as a kind of anti-insurance, or the opposite of insurance, Boyd explains to me.)

Boyd has been implementing this approach for more than a decade through the FairShares Commons, whereby individual companies structure themselves as a commons, or self-governed common pool resources (i.e., a commons of productive capacity), and groups of such companies operate as a commons of commons.

But doesn’t this kind of collaboration create antitrust concerns? Folks reading this from the United States will likely be familiar with the irrational (but politically potent) arguments of Republican lawmakers and state attorneys general that company collaboration to tackle climate change and other ecological and social crises amounts to antitrust violations.

This is a neglected but vitally important line of consideration, which is tackled by a paper released just today by the Columbia Center for Sustainable Investing that explores this question. In essence, the paper (which I was asked to review in early draft form for critical feedback) debunks the line of “reasoning” that corporate collaboration to tackle environmental and social problems is somehow forbidden by law, pointing out that the purpose of these legal structures is to protect consumers from corporate collusion that would benefit the companies at the expense of their customers. As authors Denise Hearn, Cynthia Hanawalt, and Lisa Sachs point out in the paper:

“…antitrust law is, fundamentally, an allocator of coordination rights. It defines what kind of market coordination is pro-social or benign, and where private actor coordination becomes anti-social (for example, cartel behavior).”

Collaboration to advance sustainability is clearly prosocial, as it benefits customers and companies, and furthermore, falls into the same category of a longstanding precedent of industry-level collaboration that creates a level playing field, as the authors point out.

Applying this back to the FairShares Commons, its model has proven quite successful, and one key to its success is that the individual companies do not directly compete in the same industry or sector.

So, returning to our original question, is it more advantageous to selfishly compete or altruistically collaborate? It turns out the answer is: both. This answer is not an opinion, but rather fact confirmed both by the mathematical equations describing real-world dynamics and empirical observation of living systems, which exhibit non-ergodic dynamics that optimize toward the upper limit of ergodicity.

Human systems such as business and investment are most successful when they acknowledge non-ergodicity while simultaneously structuring themselves to strive toward the upper limit of ergodicity. The best mechanism for doing so, as the ravens show us, is an optimal blend of collaboration (pooling wins and losses) and competition — this blend beats pure competition hands-down, every time, as Boyd and Reardon convincingly illustrate. This understanding is especially vital in the face of our polycrises that require massive regeneration of the planet’s carrying capacity for life. As it turns out, multilevel selection is a natural consequence of the non-ergodic nature of the real world.